One of the advantages of financial assets over physical assets is the convenience of buying and selling. For example, if you want to buy equity shares, you open a broking account and simply give an order to buy from exchanges.

As much as 40%-50% of wealth in Indian business families continues to be invested in own businesses, a trend that is unlikely to change, but there is a change in allocation with the rich preferring financial assets over physical assets, according to two recent first-of-their-kind wealth reports on high net worth and ultra high net worth individuals (HNIs and UHNIs).

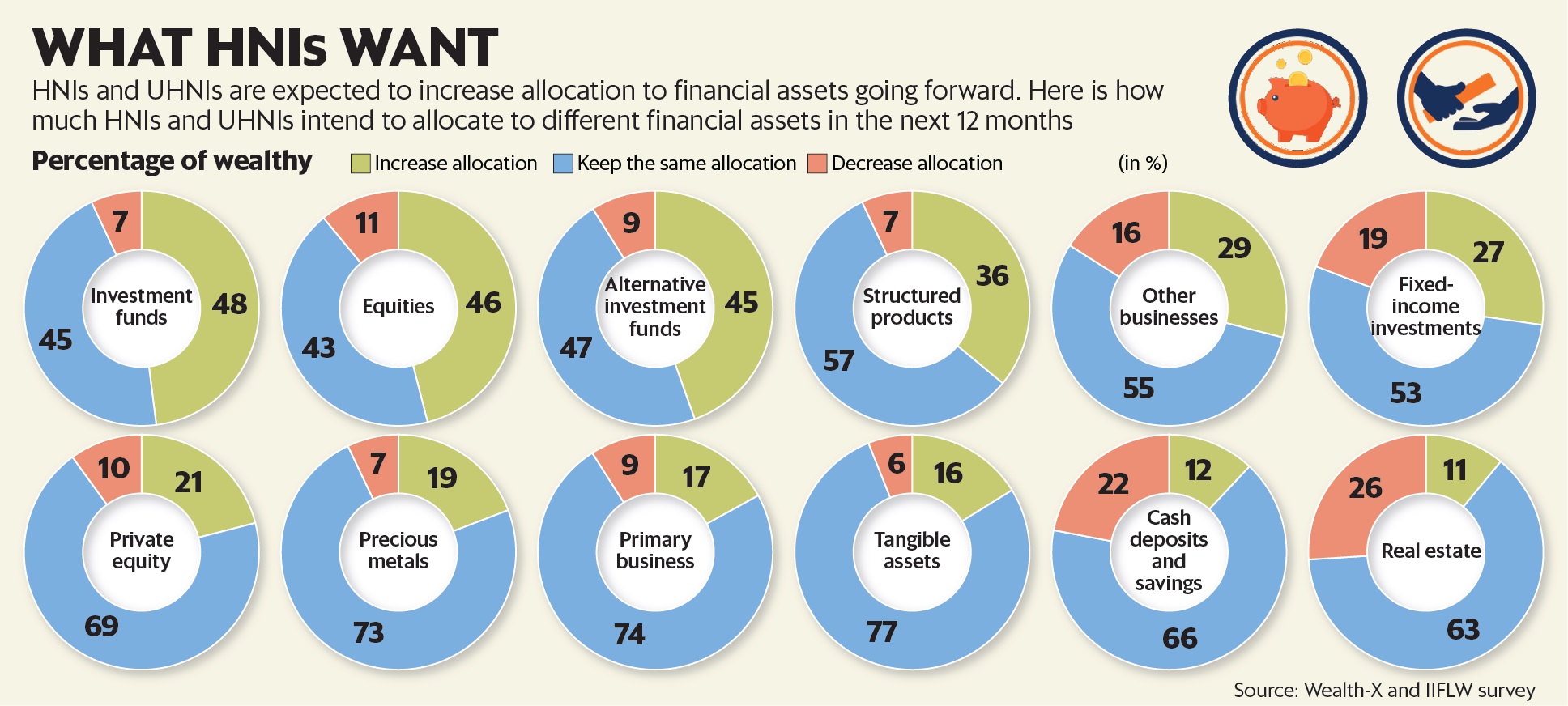

While one report, The Family Wealth Report 2018, by Edelweiss Wealth Management and Campden Research, focused on ultra-rich, family business owners, the other one, IIFL Wealth Index 2018, by IIFL Wealth Management in partnership with Wealth X, focused on the growth of HNIs and UHNIs in India along with their investment patterns. Their sample sets were different but they had a few common outcomes. Both reports found the rich are increasingly leaning away from physical assets towards financial assets. Also, both said one of the big concerns for the ultra rich is having a good succession plan.

The reports surveyed the rich, but money management has similar threads no matter what your financial status. We spoke to financial planners to ascertain whether it is worthwhile for retail investors too to have lower dependence on physical assets and focus on succession planning.

Financial assets

One of the advantages of financial assets over physical assets is the convenience of buying and selling. For example, if you want to buy equity shares, you open a broking account and simply give an order to buy from exchanges. On the other hand, buying real estate means signing several documents, getting the property registered, ensuring stamp duty payment and so on. Even buying gold requires you to tackle the issue of storage and, perhaps, open a locker with a bank.

Similarly, there is a lot more work involved in selling gold and real estate as opposed to selling shares or even a bond through your broker. For instance, finding a buyer, ascertaining the value and completing documentation as opposed to just giving an electronic sell order or signing a redemption form for financial assets.

Other than ease of operation, the costs can be especially lower in financial assets. Using managed funds like mutual funds for equity and even gold (exchange traded fund) can reduce the cost of investment. “While many do find aspects of cost and the work involved an irritant, the more important deterrent is lack of liquidity in real estate,” said Deepali Sen, certified financial planner and founder of Srujan Financial Advisors.

Financial assets are liquid. This means you are better placed to sell a financial security in an exchange-based set-up at the time you want to sell and at a price you want to sell. Sen said, “If you can’t sell a property at the price you want and at the time you want, it (the value) is just theoretical.”

Despite all the issues, real estate was a favourite for investors even a decade ago, the big driver for this shift in mindset is perhaps the lack of returns from this asset class for a prolonged period. “Thanks to the under-performance of this asset over the last 4-5 years, there is a shift in preference. Previously for investors incremental savings went into real estate but they are not keen on real estate. Things may worsen as funding to developers is unavailable,” said Tarun Birani, chief executive officer, TBNG Capital Pvt. Ltd.

“The survey found that 28% of the respondents felt they are overweight in real estate. Given the recent trends, we see more people taking advantage of financial assets going forward,” said David Barks, director, Wealth-X Custom Research, at the launch of the IIFL Wealth Index 2018. The proportion of people overweight in real estate is the highest as compared to other assets and products.

Succession planning

The IIFL wealth index points out that the richer the respondent (to survey questions), the more likely they were to set a succession plan in place. According to the Family Wealth Report quoted above, 67% of the 78 families who were part of the survey are engaging in succession planning, and 19% have a plan of some kind in place.

For retail investors living in nuclear families, a succession plan may seem a far-fetched idea. However, the idea of detailing the use of your money and assets in the event of your demise makes sense. In other words, putting in place a simple Will. “There is a definite need, however, it is one part of financial planning where I have encountered a big gap between acknowledging this need and the action required to complete it. Individuals must understand that it is not technical or cumbersome, it is about writing down how your wealth will be used in the event of your death. But perhaps there is a block when it comes to discussing in detail something like this,” said Sen.

A hand-written note detailing delegation of assets can suffice as a Will. You have to provide for what you have at the moment and mark out how assets accumulated later can be allocated. However, it is always prudent to get a formal Will drafted with the help of a lawyer and have that Will registered in a court of law.

“There are online portals too which can help in making a Will. With wealth increasing at a relatively fast pace, insecurity about the future can be addressed by making the transition smooth and a Will can do that seamlessly,” said Birani.

According to IIFL Wealth Index, over the last five years, HNI wealth has grown 37%. It also estimates an 85% growth in India’s wealthy. A growth in personal wealth automatically assigns a certain unvoiced responsibility for finances to be managed in a way that one can achieve optimum level of growth in wealth and at the same time safeguard the financial future of those who depend on your income. This applies as much to the rich and the ultra rich as it does to the average retail individual.

Read the original article:

Mint