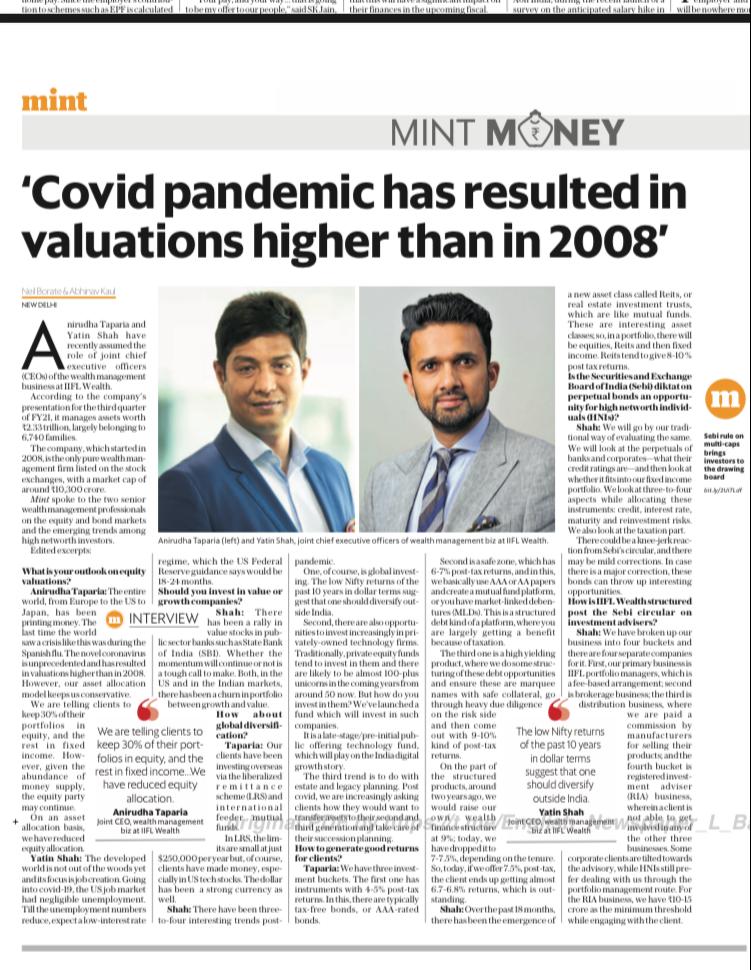

Anirudha Taparia and Yatin Shah have recently assumed the role of joint chief executive officers (CEOs) of the wealth management business at IIFL Wealth.

According to the company’s presentation for the third quarter of FY21, it manages assets worth ₹2.33 trillion, largely belonging to 6,740 families.

The company, which started in 2008, is the only pure wealth management firm listed on the stock exchanges, with a market cap of around ₹10,300 crore.

Mint spoke to the two senior wealth management professionals on the equity and bond markets and the emerging trends among high networth investors.

Edited excerpts:

What is your outlook on equity valuations?

Anirudha Taparia: The entire world, from Europe to the US to Japan, has been printing money. The last time the world saw a crisis like this was during the Spanish flu. The novel coronavirus is unprecedented and has resulted in valuations higher than in 2008. However, our asset allocation model keeps us conservative.

We are telling clients to keep 30% of their portfolios in equity, and the rest in fixed income. However, given the abundance of money supply, the equity party may continue.

On an asset allocation basis, we have reduced equity allocation.

Yatin Shah: The developed world is not out of the woods yet and its focus is job creation. Going into covid-19, the US job market had negligible unemployment. Till the unemployment numbers reduce, expect a low-interest rate regime, which the US Federal Reserve guidance says would be 18-24 months.

Should you invest in value or growth companies?

Shah: There has been a rally in value stocks in public sector banks such as State Bank of India (SBI). Whether the momentum will continue or not is a tough call to make. Both, in the US and in the Indian markets, there has been a churn in portfolio between growth and value.

How about global diversification?

Taparia: Our clients have been investing overseas via the liberalized remittance scheme (LRS) and international feeder mutual funds.

In LRS, the limits are small at just $250,000 per year but, of course, clients have made money, especially in US tech stocks. The dollar has been a strong currency as well.

Shah: There have been three-to-four interesting trends post-pandemic.

One, of course, is global investing. The low Nifty returns of the past 10 years in dollar terms suggest that one should diversify outside India.

Second, there are also opportunities to invest increasingly in privately-owned technology firms. Traditionally, private equity funds tend to invest in them and there are likely to be almost 100-plus unicorns in the coming years from around 50 now. But how do you invest in them? We’ve launched a fund which will invest in such companies.

It is a late-stage/pre-initial public offering technology fund, which will play on the India digital growth story.

The third trend is to do with estate and legacy planning. Post covid, we are increasingly asking clients how they would want to transfer assets to their second and third generation and take care of their succession planning.

How to generate good returns for clients?

Taparia: We have three investment buckets. The first one has instruments with 4-5% post-tax returns. In this, there are typically tax-free bonds, or AAA-rated bonds.

Second is a safe zone, which has 6-7% post-tax returns, and in this, we basically use AAA or AA papers and create a mutual fund platform, or you have market-linked debentures (MLDs). This is a structured debt kind of a platform, where you are largely getting a benefit because of taxation.

The third one is a high yielding product, where we do some structuring of these debt opportunities and ensure these are marquee names with safe collateral, go through heavy due diligence on the risk side and then come out with 9-10% kind of post-tax returns.

On the part of the structured products, around two years ago, we would raise our own wealth finance structure at 9%; today, we have dropped it to 7-7.5%, depending on the tenure. So, today, if we offer 7.5%, post-tax, the client ends up getting almost 6.7-6.8% returns, which is outstanding.

Shah: Over the past 18 months, there has been the emergence of a new asset class called Reits, or real estate investment trusts, which are like mutual funds. These are interesting asset classes; so, in a portfolio, there will be equities, Reits and then fixed income. Reits tend to give 8-10 % post tax returns.

Is the Securities and Exchange Board of India (Sebi) diktat on perpetual bonds an opportunity for high networth individuals (HNIs)?

Shah: We will go by our traditional way of evaluating the same. We will look at the perpetuals of banks and corporates—what their credit ratings are—and then look at whether it fits into our fixed income portfolio. We look at three-to-four aspects while allocating these instruments: credit, interest rate, maturity and reinvestment risks. We also look at the taxation part.

There could be a knee-jerk reaction from Sebi’s circular, and there may be mild corrections. In case there is a major correction, these bonds can throw up interesting opportunities.

How is IIFL Wealth structured post the Sebi circular on investment advisers?

Shah: We have broken up our business into four buckets and there are four separate companies for it. First, our primary business is IIFL portfolio managers, which is a fee-based arrangement; second is brokerage business; the third is distribution business, where we are paid a commission by manufacturers for selling their products; and the fourth bucket is registered investment adviser (RIA) business, wherein a client is not able to get involved in any of the other three businesses. Some corporate clients are tilted towards the advisory, while HNIs still prefer dealing with us through the portfolio management route. For the RIA business, we have ₹10-15 crore as the minimum threshold while engaging with the client.

Read the original article:

Mint